MDR :

The monetary policy announced by RBI last week was yet again proved to be nugatory, with the committee deciding to hold interest rates. But the decision of RBI to rationalize the MDR on debit card transactions from 1st January, 2018added a bit of briskness to the proceedings.

What is MDR?

Merchant Discount rate (MDR) is the rate charged to a merchant by a bank for providing debit card services when payment is made at a merchant point of sale (PoS). More often than not, such charges are passed on to the customer by the merchant. Therefore a rational customer would prefer not to opt for non-cash transaction as cash transactions have no such additional costs.

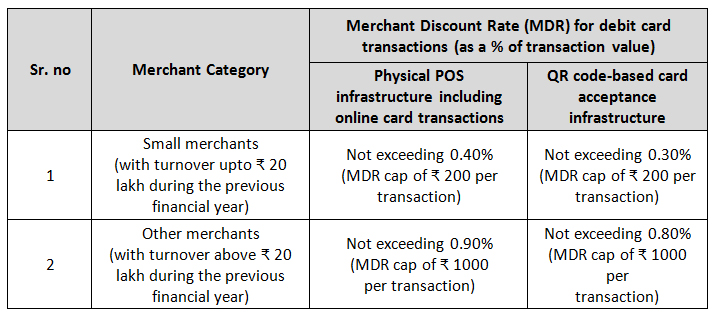

As per the RBI’s notification, the revised maximum MDR for debit card transactions shall be as under:

Importance:

It has been a challenge to convince small merchants to install PoS machines as it entails additional cost and burden. On the other hand, Banks are willing to extendPoS coverage only if the share of MDR is more lucrative to them.

With an attempt to resolve this tug-of-war between merchants and bank, RBI’s latest moves allows banks to charge higher fee from large merchants and allowing the smaller merchants to pay nominal fees.

The Impact:

Earlier, MDR fee was charges based on the bill value. A fee of 0.25% was levied on bill value upto 1,000 INR, 0.5% for transactions between 1,000 and 2,000 INR and 1% for transactions above 2,000 INR. But after 1st January, every transactions with big merchants will attract a 0.9% MDR.

So, while your neighborhood Kirana store or general store may acquire a brand new PoS machine, the large merchants may nudge you to use cash for small transactions.

Moreover, to encourage the use of debit cards, government announced that it would reimburse MDR on transactions upto 2,000 INR for next 2 years starting 1st January, 2018, which is a welcome move.

The Issue:

As the retail business, especially a supermarket or hypermarket, which operates with a margin of around 2-5% such an increase in MDR will have a huge impact on costs.

Amrish Rau, CEO of PayU, in a tweet, said that- though the RBI has again tinkered with Debit charges. The problem is NOT MDR. To provide big boost to digital payments, capping of Bank interchange fees is a must. Such fee is charged by Issuing banker (0.5-0.75%), Recipient Banker (0.5-0.25%) which is shared alongside the payment service provider such as Visa/ Mastercard.

Bottom-line:

Net- net with both, Merchants and bankers trying to figure out cost benefit and RBI putting in policies and efforts to reduce cash transactions, it isn’t clear if the revised MDR charges would encourage usage of plastic money.

Author

![]()